This is not a blog entry. Instead, it is a white paper I have produced in my line of work as General Partner at Accelerace Invest and Overkill Ventures. But I post it here to log advances in my thinking.

Disclaimer

The theory, framework, and tools provided in this white paper are not attempts to create an exhaustive evaluation framework regarding investment decisions in startups. The focus of this paper is purely to assess the potential speed of growth. For most investors, the speed of growth is just one of many factors that investors must evaluate. Among these are: the quality of the team, the terms of the deal, and the momentum of startup. For the last part we recommend reading the white paper called Momentum from the same authors. The Momentum white paper can be found on here.

Prelude

Since 2009, Accelerace has seen hundreds of startups unfold their full potential. Some have become unicorns and others have become lifestyle businesses. The ability to track these companies over a decade, has given us insight into different growth stories. Stories we extract lessons from and transform to processes at our accelerator programs and VC funds.

From some of our earliest cohorts, two companies stood out. Both were courted by big name VCs and received tickets to shoot for the ultimate outcome. The reasons were obvious. Both startups found early product-market-fit, had little competition, and were targeting massive market opportunities.

Twelve years later, the two companies have unbelievable different growth stories. One employs more than 1,000 people. The other counts about 30 people. The first has a valuation of about 1.5 billion USD. The other about 25 million USD.

Why did they grow at such different speeds?

At first glance this is puzzling. Both companies attracted a stellar team, board, and investors. In addition, they received equal portions of seed capital.

Upon a second look, the answer becomes obvious. But it requires the lens provided by two concepts to unfold. We call them: Beta and Alpha.

Introduction

Venture capitalists and startup founders focus on growth. The reason is simple. Growth is synonymous with success in the world of startups. But to venture capitalists, growth is only half the story.

For venture capitalists, the speed of growth is even more important. The reason is that VCs measure their return in IRR (internal rate of return). Simply put, a 10X return is worth more than double if achieved in 5 years rather than in 10 years.

But how can one assess if a startup has the potential for rapid growth?

Today, we have come to understand the potential speed of growth of any company to be defined by two factors.

- One, the growth of the market for the service/product: Beta

- Two, the relative competitiveness against competitors in the same market: Alpha

Beta and Alpha will be illustrated below with a simple and fictional scenario of two startups. BlueApp and RedApp.

The effect of Beta

To illustrate Beta, we can imagine two startups: BlueApp and RedApp with identical value propositions. Let us imagine that these two startups target the same market of 10 potential customers interested in the product category that these startups offer. Next year, the number of customers grows to 20. And the following year, the number is 40. Put differently, the market grows 100% per year. This would be an attractive Beta for most companies.

In this example, both BlueApp and RedApp should start out with 5 customers each. The following year both startups have 10 customers. The following year, they both have 20 customers. The scenario is illustrated by the graph 1 below:

As we can see on the graph above, both startups grow 100% per year. The scenario could be called: “Attractive Beta, No Alpha.” That is because the market grows 100% per year, but there is no difference between the strength of their value propositions. In short, this means that each startup grows at the rate of the market. With no Alpha, the growth of a startup is simply defined by the market growth. Or if applying our terminology; by the Beta.

And here is the first hint at our mystery outlined in the Prelude. The startup valued at 1.5 billion USD operated in a market with incredibly attractive Beta. The other startup was in a market with zero Beta. The first startup entered a market just about to take off and the market would keep growing rapidly for the next decade. The other startup entered a market with no growth. Consequently, every customer had existing routines, alternative solutions and existing vendor relationships. Importantly, even though the startup valued at 1.5 billion USD had a much smaller market to begin with, this would soon change.

The effect of Alpha

Rarely do companies differ in name only. To make the example more realistic, let us imagine that only RedApp has an algorithm based on user data that improves the app. This would be a rather attractive Alpha for RedApp.

The first year, the startups share the market with 5 customers each. But the following year, the 5 customers of RedApp has improved the dataset behind RedApp’s algorithm. Now, RedApp’s value proposition is superior. Consequently, most new customers on the market prefer BlueApp. Now RedApp has 15 customers that help improve the app. In year three, most new customers also choose RedApp. And so, it continues. In other words, RedApp has a Reinforcing Value Loop that spins at an increasing pace, meaning that BlueApp cannot keep up.

The scenario is illustrated by the graph 2 below:

As illustrated on the graph above, Beta and Alpha both influence the growth of BlueApp and RedApp. The scenario could be called: “Attractive Beta, Attractive Alpha for RedApp.” That is because that even though the market grows with 100%, RedApp grows significantly more than 100% a year, whereas BlueApp grows less than 100% a year.

And here is the second and definitive answer to our mystery outlined in the Prelude. The startup valued at 1.5 billion USD did not only have attractive Beta. It also had an incredibly attractive Alpha. Every new user improved their app, and past a certain point, competition was irrelevant. In contrast, the other company enjoyed neither Beta nor Alpha.

Sources of Beta

In the previous section we made Beta synonymous with the growth of the market. However, this was a simplification.

In fact, Beta comes from a combination of two sources. First, the rate of new customers to the market. Second, shifting preferences among the customers in the market.

We define the market as the buyers and sellers engaging in transactions of a product category.

We find that the rate of new customers to the market is the clearest source of Beta. If considerable amounts of new customers enter the market every year, there are a vast number of willing buyers with no existing vendor relationships to sell to. And even though a startup faces competition, the number of new customers can be so large that competitors are preoccupied with servicing their own part of the growing market.

On rare occasion, extremely high rates of new customers appear. Often, this is due to radical innovations that provide a leap in value or/and lower costs for customers. In these cases, markets are “unlocked” and floods of new customers appear seemingly overnight. That was true for short term apartment rentals that were “unlocked” by Airbnb. Consequently, the rate of people wanting to rent out their apartment exploded.

Other examples of strong rates of new customers include: The rise of mobile developers during the late 2000s (caused by the iPhone) and explosion of delivery focused restaurants in the early 2020s (caused by Covid). Companies that benefitted from those examples include Unity Technologies and Wolt.

Another source of Beta is shifting preferences among customers. Regardless of the rate of new customers, the preferences among the existing customers can shift. If a startup is positioned to benefit from this shift, it can win customers as a result. A recent example is the preference for recruitment tools that ensure non-biased hiring. The number of corporate HR managers is stagnant. However, their preference is shifting. Consequently, startups that offer recruitment tools with candidate anonymization, could experience rapid growth driven by this source of Beta.

Real life examples of shifting preferences among customers include: The shifting consumer preference towards craft beer in the late 2000s. Corporate preference towards consumer style communication tools in the mid 2010s. Companies that benefitted from those examples include Mikkeller and Slack.

Obviously, the most powerful form of Beta comes from the combination new customers and shifting preferences. If the rate of new customers to a market is rapid and the preferences among customers in the market is shifting to the benefit of the startup, one has a cocktail for explosive growth. An example of such a cocktail was review management for online shops in the late 2010s. This period was marked with an explosion of new webshops. At the same time, these webshops increasingly started using reviews in their marketing. A company that enjoyed this “Beta cocktail” was the review site Trustpilot (Accelerace alumni 2009).

The five levels of Beta

As outlined above, Beta comes from two sources. And various combinations of strengths of these two sources lead to varying strengths of Beta.

Accelerace has developed a classification system for different strengths of Beta. The levels are easily identifiable by their combination of the rate of new customers and the shifting preference among customers. The right-hand side provides further details to aid with accurate classification.

When classifying a startup, it is important to note that the classification should not be based on historic dynamics. Instead, the classification must forward oriented. That is because startups benefit from the growth to come, whereas previous market growth is mostly irrelevant.

Naturally, the future is impossible to predict. Consequently, investors must classify the startups according to a qualified estimations of the rate of new customers and the shifting preference among customers.

The levels can be seen below. The scale goes from level 1 (weakest) to level 5 (strongest).

| Level 1 Beta | The startup faces: Slow rate of new customers. & Slow shift in preferences among customers. | In this scenario the number of customers in the market is almost stagnant. Furthermore, the customers are not increasing their budgets or buying activity for the type of product category the startup sells. This is the lowest level of beta and makes it difficult for a startup to grow. An example could be cash handling POS systems for canteens. The number of canteens is not growing. And few canteens are looking to buy POS systems that can handle cash. |

| Level 2 Beta | The startup faces: Slow rate of new customers. & Steady shift in preferences among customers. | In this scenario the number of customers in the market is stagnant. However, the customers are increasingly interested in buying the product category that the startup sells. This is still a low level of beta because the customers often have existing vendor relations and will ask their vendor to supply the new product. Examples would be digital security camara systems for public parking. The number of public parking spaces is almost stagnant, but many are looking to upgrade their existing security systems. But because they have bought security systems for years, the existing vendors will fill most of this demand and leave little room for startups. |

| Level 3 Beta | The startup faces: Steady rate of new customers. & Steady shift in preferences among customers. | In this scenario the number of customers in the market is growing steadily. Furthermore, the customers are increasingly interested in buying the product category the startup sells. This is an attractive Beta because the new customers will have no existing vendor relations and startups have a more “level playing field”. Examples would be mental health apps. The number of people who engage in mental health is growing steadily. In addition, these people are increasingly using digital tools rather than just attending physical classes and treatment. |

| Level 4 Beta | The startup faces: Steady rate of new customers. & Rapid shift in preferences among customers. | In this scenario the number of customers in the market is growing steadily. However, the customers are rapidly adopting the product category the startup sells. This is an attractive Beta because the market has new customers with no existing vendor relations which gives startups a more “equal playing field”. Furthermore, the strong shift in preferences among customers means that many of the existing vendors cannot innovate fast enough, and startups can swoop in. Examples would be many Fintech products. The number of people who seeks to administer their finances is growing steadily, and people are no longer seeking financial advisors and banks to scratch this itch. Instead, they rapidly seek digital tools. |

| Level 5 Beta | The startup faces: Rapid rate of new customers. & Rapid shift in preferences among customers. | In this scenario the number of customers in the market is growing rapidly. In addition, the customers are rapidly adopting the kind of product the startup sells. This is an extremely attractive Beta because the market has many new customers with no existing vendor relations which gives startups a “blue ocean”. Furthermore, the strong shift in preferences for the benefit of the startups means that many of the existing vendors cannot innovate fast enough, and startups can swoop in. Examples would include digital collectibles. The number of people who seeks to collect digital items are exploding. In addition, the blockchain– |

Sources of Alpha

Alpha describes outperformance by a startup relative to the market growth rate. However, as investors we need to estimate the future growth rate. This means that we must understand the sources of Alpha.

At Accelerace we find that the only lasting source of Alpha originates from Reinforcing Value Loops (RVLs). A RVL is in place when the product increases in value with each new customer. Thereby, the loop is “reinforced” with each “spin”1.

The most obvious form of RVL comes from network effects. Marketplaces tend to enjoy RVLs because each new user adds goods/services that increase the value of the marketplace to new users.

However, we find that network effects are just one of various sources of RVLs. RVLs can also stem from economies of scale, where higher volume increases the value of the product. A classic example is deal sites. If they get more users, they can negotiate better deals, which in turn attracts more users.

Another potential source of Alpha is data. The more users, the more data is generated, which can be used to create a better product experience for new users.

The authors are not blind to other sources of Alpha than those that stems from RVL. Such as unique access to key people, superior know how, special rights, etc. However, we find that these are short lived and that RVLs are the only sustainable source of Alpha.

The five levels of Alpha

As outlined above, the only sustainable Alpha comes from RVLs. And various types of RVLs lead to varying strengths of Alpha.

Accelerace have developed a classification system for different strengths of Alpha. The levels are easily identifiable by their combination title. The third column provides further details to aid with accurate classification.

The levels can be seen below. The scale goes from level 1 (weakest) to level 5 (strongest).

| Level 1 Alpha | The product is one where: Customers legitimize the product. | The startup has a product that introduces a new way of doing things. Most customers are waiting for other customers to use the product before they take the jump. Consequently, it becomes easier to sell as more customers buy because potential customers increasingly regard it as a legitimate solution. This is a low level of Alpha because legitimacy can take a long time to build due to the laws of the technology adoption lifecycle. Examples would include Bitcoin. Many people want to be sure that Bitcoins are valid assets before engaging themselves. |

| Level 2 Alpha | The product is one where: Customers enable the product. | The customers make it possible to offer the product because a certain scale is required. Thus, the more customers the startup gets, the better product experience they can offer. This is a decent level of Alpha because it has elements of network effects. Examples would be deal sites and collaboration tools. Unless a certain number of people use the deal site, the deal site cannot make good deals with shops. And unless a collaboration tool has enough users, the tool has no value. However, at a certain scale this effect has diminishing returns. |

| Level 3 Alpha | The product is one where: Customers contribute to the product. | The customers create part of the content that is offered to new customers. That could be valuable data, templates, and creations. This is a strong level of Alpha because the customers are directly affecting the value of the product. Examples would be template-based design tools (like Canva). Here the users are creating designs and templates that can be added for new users. |

| Level 4 Alpha | The product is one where: Customers create the product. | The customers create the key content that is offered to new customers. That could be valuable data, templates, and creations. This is a strong level of Alpha because the customers are directly creating the value of the product. Examples would be review apps (like Vivino). Here the users are creating the key content that other people are seeking. |

| Level 5 Alpha | The product is one where: Customers are the product. | The customers are the product. This is the most extreme form of Alpha because it is pure network effects. Examples are dating apps and social media. Once a startup gains a head start in accumulating users, their Reinforcing Value Loop will spin so fast everyone else will be left in the dust. |

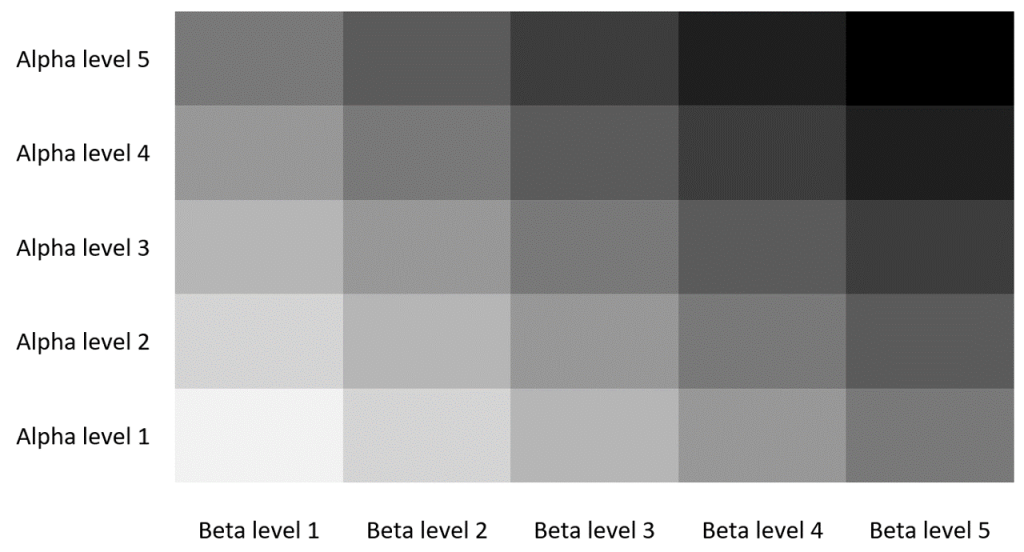

Beta and Alpha combinations

Both Beta and Alpha define the growth potential of a startup. However, startups do not need high levels of Beta and Alpha simultaneously to grow fast. In our experience, a high level on one is enough.

In cases where a startup enjoys high Beta but limited Alpha, the startup can still monopolize the rapidly growing market through sheer execution and operational excellence. In cases where the startup enjoys high Alpha but limited Beta, the startup can win most of the customers in the market by providing a much better product than competitors.

In the table below, we have illustrated the various combinations of Beta and Alpha possible. The darkness of the color indicates the attractiveness of the combination.

As illustrated in the table above, the highest potential for rapid growth is found in the upper right corner. Here startups are defined by high levels of Beta and Alpha simultaneously.

One would be forgiven to think this means that investors should focus on social media and dating apps because these products have level 5 Alpha. However, the authors stress that this would be a faulty interpretation. The table merely shows that such startups have the potential to grow faster than startups with low levels of Alpha. Whether this potential is realized is another story.

Beta and Alpha in use

We suggest classifying all investment candidates with Beta and Alpha assessments. This can be done by whomever scouts the startup because the classification system should enable anyone to accurately assesses Beta and Alpha levels of investment prospects and enrich the pipeline tool with this data.

In addition, Investment Managers and Partners can use the tool to enrich their investment proposals with these assessments. This will enable the Partners and/or the Investment Committee to use a shared taxonomy when discussing the growth potential of the companies in question.

Another use of Beta and Alpha classifications is for acceleration or “value-add” purposes. Investment Managers, Board Members, and Advisors can use the classification to aid portfolio companies with strategic decisions. Taking Beta into consideration is useful when doing segmentation and contemplating go-to-market strategies. Taking Alpha into consideration is useful when discussing strategic product directions because some features could add elements of Alpha.

At Accelerace we use the Beta and Alpha classification in our Investment Proposal document template. Investment Managers assess the Beta and Alpha levels of an investment candidate and present this assessment to the Investment Committee (IC). Because the IC members understand the classifications, we find that the discussions about the potential speed of growth of companies become radically more effective.

As can be seen on the screenshot of our Investment Proposal document template below, Beta and Alpha scores are requested in the section: Investment Conviction and Forecast.

In addition, we teach Beta and Alpha as topics in our acceleration programs. We include courses on Beta and Alpha and have design tools to help the startups design RVLs. We find that teaching these concepts and addressing potential scaling issues becomes much easier and more effective using this classification.

Limitations of the model

Naturally, there are limitations to the Beta and Alpha model. The most important are:

- Beta and Alpha levels have little predictive power for the outcome of an investment. Investment outcomes are influenced by a myriad of factors including macroeconomic circumstances, trends, legislation, competition, team etc. For this reason, it is easy to identify examples of companies with high Beta and Alpha that fared worse than certain companies with low Beta and Alpha. That said, Beta and Alpha are defining of the potential outcome at the time of the investment.

- The model does not define the potential size a startup. A company can continue to grow over generations, as have been the case with companies such as Disney and Coca Cola. The model only addresses the potential speed of growth.

- With just five levels of Beta, there are combinations of Beta scenarios that are not included. E.g., Stagnant rate of new customers & Strong shift in preference among customers. The scenarios that are not included are rarer and the authors have chosen to prioritize simplicity over exhaustiveness. That said, the model could be expanded to include all scenarios.

- There are sources of Alpha that are not included in this model. Many of these are what investors would call “edges” or “unfair advantages.” That could be know-how, personal relations, unique access to resources etc. All of these would make a startup grow faster than the market rate. However, these types of Alpha are often unique and unsustainable. Thus, we have not (yet) been able to classify these. Consequently, we suggest evaluating these on a case-by-case basis.

Implications

First, Beta and Alpha allow for quantitative evaluation of the growth potential of investment candidates. This is useful when communicating and discussing this aspect during partner meetings and IC meetings. Furthermore, they allow for clear communication between decision makers and the scouts that often perform the initial assessment of startups. With this tool, one could easily imagine scouts being given the brief to look for startups with “Beta levels above 3” and “Alpha levels above 2”.

Second, the model enables quantitative analyses of past investment decisions. If the Beta and Alpha levels are recorded, it is easy compare these scores with actual perform and use this to optimize the investment decision tools.

About the authors

Peter Torstensen and David Ventzel are partners at Accelerace. Accelerace is a startup accelerator and VC placed in Copenhagen Denmark. Accelerace was founded in 2009 and have accelerated more than 700 startups to date.

The authors have been aided by their Head of Acceleration, Mads Løntoft and Peter Marculans, Managing Partner at Overkill Ventures in the development of this paper.

Contact

If you are interested in the model and collaborating further development of the framework, then contact David Ventzel: dav@accelerace.io.