Accelerator programs will connect you to venture capital firms. This post will not. Instead it will do the opposite. It will distance you from venture capital. The distance will allow you to understand them. In the process I will tell you a personal story. I will over-generalize and simplify venture capital. I will even blame Warren Buffett. But in the end you will understand VCs. Understanding is power. Use it.

Most founders pitch to venture capitalists. Founders think they should. VCs exist to fund startups. Everyone knows this.

But this is not what most founders experience. Founders experience something like this: They got a startup. The team is good. The product is good. They have customers. They even got angel investors. But VCs don’t invest. So why don’t they invest?

I used to be puzzled myself. As a founder I thought they didn’t get my idea. They didn’t believe what I believed. They didn’t believe in me. I felt rejected. It hurt. I smashed my bike into a tree while being on it. Then I met someone. He was miserable. But that meeting changed everything.

I became an investor

But before this meeting something else happened. I got offered a position at Accelerace Invest. I became Investment Manager in a micro VC fund of €35 million. We invest in startups graduating our accelerator programs.

I started understanding the investment side of the game. We aren’t really a VC though. We can only do seed investments. The “real” VCs still puzzled me. That was until the day I received a mail from LinkedIn.

It was an auto generated mail. But it caught my eye. It said that a friend had gotten a new job. He was now VP in a top 3 venture capital firm. I called him. He was excited. It was a dream coming true for him. He was mistaken. But it took two years before he learned.

The napkin that changed everything

I met him in London. It was rainy. The weather fitted his mood. He was miserable. With a tired voice he told me: For the past two years he had not invested in a single startup. I was shocked. What!? For two years he had been doing nothing!?

Then he told me something that made all the pieces of the puzzles fall in place. Suddenly all the rejections from VCs I received as founder made sense. Now I knew. I felt at peace. It was awkward it the midst of his misery.

He explained that his firm manage multiple funds. He was investing out of a €100 million fund. He told me that it was a 10 year fund. They spend the first five years investing. The remaining five years they try to exit the companies. I knew how this worked. Almost all venture capital firms have 8 or 10 year funds and operate this way. It was the next thing he told me that really opened my eyes.

He told me that the LPs (the investors in their fund) expect 20% in annual gain. The gain is called Internal Rate of Return (IRR). Simply put, they expect the fund to increase in value 20% every year.

It made sense. I knew that good hedge funds generate 20% return per year. Warren Buffett has generated 20% on average the last 50 years. Naturally, the partners of the VC fund promise the same return. If not, the LPs will give the money to Warren Buffett.

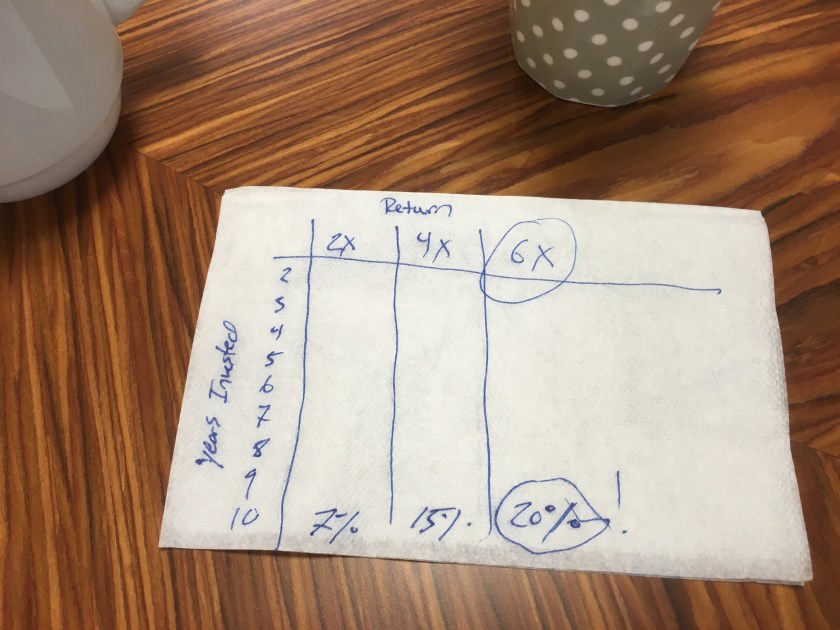

My friend grabbed a napkin. He furiously started drawing a table with numbers. He almost seemed like a mad man. He asked me: Do you know how much 20% every year for 10 years is!? Do you know how much money we must return to our LPs!? I looked at the napkin. I found the intersection between year 10 and 20% IRR. It said 6.

6 times! We need to return the money 6 times, he said, while throwing the napkin up in the air. In other words, he had to turn €100 million into €600 million. If not, Warren Buffett gets the money. No wonder he looked tired.

But something bothered me. If he was under so much pressure, then why didn’t he invest like crazy? It made no sense. If he only had 10 years to turn a €100 million into €600 million, then why had he not invested yet? Actually he only had 8 years by then. I could almost feel his stress.

But I already knew the answer. This part was no different from my job at Accelerace Invest. We have the same problem. The problem is math.

One startup to rule them all

Most startups fail. They either go under or become zombies. A zombie can feel like a success to a founder. The startup grows into 10 to 30 people. Maybe it makes a little profit. The founder has built a company. But it doesn’t hyper scale. In the eyes of an investor, it’s a failure. A zombie. The truth is that only 1 out of 10 startups hyper scale. No hyper scale means no IPO or exit to Google. The money is stuck. It’s a nightmare for investors. Imagine you couldn’t withdraw your money in the bank.

The problem is this: The one startup that exit must single handily make the 20% annual return. The fund must make €600 million on the sale. A VC typically owns a 1/3 at exit. That means the startup must exit for €1.8 billion. And in less than 10 years. Actually down to as little as five years for investments done in year five.

Suddenly everything made sense. Why I had been rejected so many times as a founder. It wasn’t because the VC didn’t get it. It wasn’t because the VC didn’t believe in me. Admittedly that might have been a factor. But probably, math was the main problem. I hadn’t made it clear how my startup could exit at €1.8 billion in a few years. I didn’t know that I was supposed save his fund from being outperformed by Warren Buffett. I just thought we should grow and make profit. I didn’t know. Most founders don’t.

I looked at my friend with an expression of understanding. I picked up the napkin from the floor. It’s hard to find a startup that can return that much money in so little time, I said. That is why you haven’t invested yet. He nodded. So hard, he said, while falling back in his chair. It turned out being a venture capitalist wasn’t fun after all. He just wanted to help founders. Suddenly I felt I had the better job.

Think twice

Before you open your pitch deck to correct your exit slide, stay with me. It is not about convincing the VC that you can save his fund. It’s not about the VC at all. It is about you.

Do you really want to play the VC game? Does your startup truly have that kind of DNA? If you do. A VC can turn you into a unicorn. You can become Mark Zuckerberg. If not, the math behind a VC will crush you. I have seen it happen. Many times. And I am planning to write about it. To illustrate what happens to a startup when VCs invest. What happens if the startup doesn’t really have that DNA. If you want to read that post, keep an eye on my blog.

Conclusion made:

- VCs compete with other fund managers, including Warren Buffett…ouch!

- VCs want you to make the entire return of the fund in a very few years

- VC funding is only for a very few types of startup and founders