Books and lawyers will teach you the art of negotiation. This post will not. Instead it will deconstruct the equation behind valuation. It will expose the different elements and weight them. The equation will give you knowledge to optimize your valuation. Knowledge is power. Use it

Most founders want a high valuation. It’s on the last slide of the pitch deck. They meet the investor and pitch energetically. They get to the last slide, pauses and say the big number. They look the investor straight in the eyes. The room turns silent. They think it’s all about being confident. To look like they are worth it. I used to think so too. Now, I know better.

Getting a high valuation is not like a Turkish bazaar where starting high and expecting half pays off. The truth is that valuation is tricky. In fact, it’s downright peculiar. After 3 years of startup investing and raising funding for about 14 startups, this is what I know:

Valuation is not value

Valuation indicates “value”. It’s a poor choice of word. It has little to do with value. I once talked to founder. He told me that an investor had given his startup a €2 million valuation. He said that he was a millionaire because his startup was worth €2 million. He was wrong.

Valuation is not value. Value is something a buyer assigns to an asset. Investors are not buyers. They don’t want to buy. They want to sell. They are investors. If they wanted to buy, they would want a majority of the shares. They don’t. In most cases, startups don’t have any value. None wants to buy it.

Then what is valuation? Valuation is distribution of shares. It calculates how many shares the investor receives. That’s it. Does this matter? Certainly! But, not as much as founders think.

Only two things really matter: 1) how much influence the founders have 2) how much money founders get in an exit scenario. None of them are a direct function of the share distribution.

Instead, influence is a function of the rights assigned to the particular shares. It’s possible to have large shareholders with limited influence. It’s also possible to have small shareholders with significant influence.

How much money founders get in at exit a function of the price of the company, liquidation preferences assigned to specific shareholders and the amount of shares held. Two of the three elements are detached from the distribution of shares.

Conclusion: valuation matters, but not very much.

What valuation actually is

Valuation is not that important. But founders still want a high valuation. It feels good. It’s a vanity number. It influences the morale of the team, the chance to be featured on Techcrunch and the level support from the family. Valuation is social capital. Human hierarchies are formed by social capital. In that context, valuation is important.

Conclusion: Valuation is primarily social capital

The limits of valuation

Getting a high valuation depends on more than just the haggling. If founders understand what those things are, they can increase their valuation. If founders know which things matter the most, they can maximize it.

What matters and how much below:

The first thing founders should know is this: The valuation has limitations. Not because investors have a sense of fairness. But because (institutional) investors have specific investment strategies.

Investment strategies restrict investors. In practical terms, it means that investors aim to own a specific amount of the company and invest within a certain size frame. This mathematics defines the limitation of the valuation. Any valuation not fitting this math is impossible for investors to accept.

At Accelerace Invest we often meet founders who ask for amounts we simply don’t do. The reason is that investors have investors. And the investors of the investor don’t like to see their asset managers go rouge. Many founders don’t know this.

Conclusion: founders should understand the investment strategy of the investor because it governs the limitations for the valuation.

Getting the maximum valuation

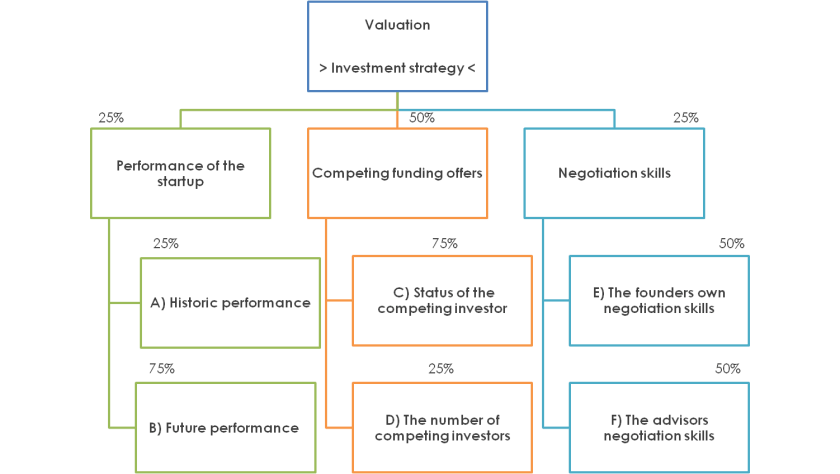

Maximizing valuation is basically a function of three things. 1) Performance of the startup, 2) competing funding offers the startup has received (term sheets) and 3) negotiation skills

1) Performance of the startup is a function of A) the historic performance of the startup and B) the future performance of the startup.

2) Influence by alternative funding offers are a function of C) the status of the competing investors and D) the number of competing investors.

3) Negotiation skills are a function of E) the founders own skills and F) the skills of the advisors they use.

Now that we identified the variables, let’s assign the weights.

What is most important? 1) The performance of the startup, 2) the competing funding offers or 3) the negotiation skills?

The obvious answer is the performance of the startup. If the startup makes a ton of money, the company is really valuable. Right? Yes and No. The problem is that some startups get a really high valuation with no significant traction.

The second obvious answer is negotiation skills. Being confident and having the right arguments. Right? In combination with stellar performance, negotiation skills will work in your favor. Without traction, confidence and arguments seems delusional.

What about competing funding offers? Are those important for valuation? Experience tells me that they are. In fact, they often trump everything else. If investors flock around a startup, the game changes. I’ve seen it. It happened to a few startups I helped. Their fundraising were no longer a game between the founders and the investors. It became a game among the investors.

With multiple investors in play, the game turns social. Some investors are friends. Some are not. Some have a low status and other have high status. Played right, this game can work in the favor of the founders.

Founders can get investors to compete, bid and form alliances. Suddenly the main argument for investing can be: “this really well-known business angel or VC fund is investing at this valuation”. Suddenly, the valuation is detached from performance or negotiation skills. It is driven by the game investors play among each other.

Conclusion: competing funding offers are essential for maximizing valuation.

Conclusions made:

- Valuation matters, but not very much

- Valuation is primarily social capital

- Founders should understand the investment strategy of the investor because it governs the limitations for the valuation

- Competing funding offers are essential for maximizing valuation

One thought on “The equation of (seed stage) valuation”